From: https://www.davidstockmanscontracorner.com/wtf/?mc_cid=a44ca768dd&mc_eid=23bf5d4e64

WTF!

WTF!

Washington has well and truly lost what little collective mind it had left. Its panic driven assault on financial sanity apparently has no limits whatsoever, which means there will be hell to pay when trillions upon trillions of mindless monetary and fiscal “stimulus” comes flooding into an already debt and speculation enfeebled economy now being shocked by the Covid-19.

With five US Senators already quarantined, perhaps we will be spared for a few days the insanity of the $1.6 trillion Everything Bailout. It got hung on a 47-47 vote Sunday evening, and then stymied again today by 49-46, when 60 votes are needed to close debate.

This is shades of the first TARP vote in September 2008, which caused Wall Street to puke and the so-called GOP “fiscal conservatives” to fold their tent.

But this time it looks like the House Dems have their number. If the GOP fiscal hypocrites want to raid the US Treasury to fund their 2020 election campaigns, then the Dems have just put a $2.5 trillion alternative package on the table—with a helicopter check of $1,500 for every man, woman, child and they in America.

Holy moly, let the auction of America’s remaining bit of fiscal solvency begin!

To be sure, it may take the duopoly a week or even longer to agree on how to divide up the loot between their various constituencies and the Red and Blue state geographies, but in the interim the fools in the Eccles Building have their back.

The Fed can apparently be operated by telephone, or even smoke signal if need be. So come rain, shine or quarantine, it means to stay on the rampage.

In this morning’s announcement, in fact, the Eccles Building basically said it is “open to buy” or refi every single kind of debt ever invented by Wall Street, and at ultra-low, deeply subsidized rates.

This was all gussied up in risible Fedspeak about providing “powerful support for the flow of credit to American families and businesses”.

But that’s complete humbug. The essence of today’s action is the final euthanasia of interest rates in the American economy. Henceforth there will be zero honest price discovery, which will be supplanted instead by FOMC dictated rates and spreads.

We call attention especially to this morning’s mind-boggling announcement that the Fed is standing up two massive corporate debt buying facilities (one for primary issues and another for existing bonds), and for exactly why?

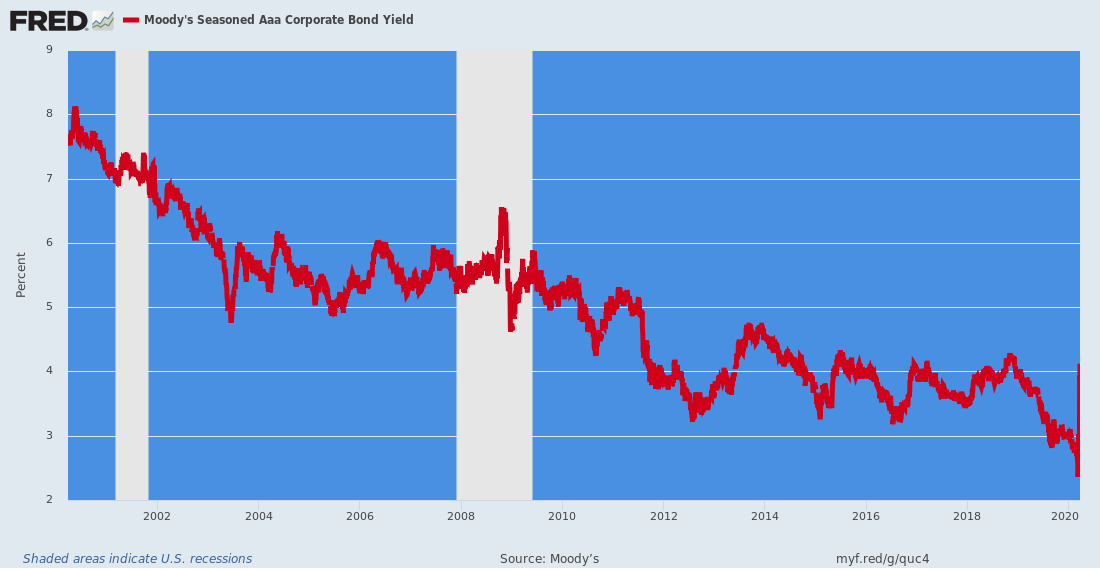

Here [below] is the last twenty years of the Aaa corporate bond yield, and it fairly screams out: Where’s the fire!

After all, the yield hit a preposterous all-time low of 2.36% on March 6th. That happened to equal the Y/Y core CPI rate, meaning that the real cost of new Aaa corporate debt was, well, nothing!

However, as of late last week the yield had spurted to 3.86%, which is still well below where it has been for most of the last 20 years. Yet the crybabies in the corporate C-suites, who have spent most of this century shit-canning their own balance sheets to fund mostly destructive financial engineering, apparently could not countenance the prospect of paying 4% to borrow new money.

Actually, what’s wrong with the 6% or even 8% corporate bond yields which, as shown in the graph below, were par for the course before 2008?

Here’s the thing. This isn’t about

1. investment grade debt availability or

2. “credit flow” to business or

3. a bond market that has stone cold shut down.

Instead, it’s about

1. the carry cost of debt-bloated corporate balance sheets.

Last week a record $35.6 billion flowed out of corporate debt funds, but that simply means under current circumstances that most of these outflows went into cash. And they will only come back into the corporate bond pits upon a sharp upward reset of yields designed to compensate for the suddenly rediscovered reality of risk.

Of course, there is only one thing wrong with letting price do

its job and allowing the corporate bond market to clear pursuant to the laws of

supply and demand. To wit,

it would result in a heavy hit to earnings,

share prices and executive stock options!

Stated differently, in a world awash with speculative capital this is about profits, not funding availability.

Indeed, that’s the real evil fostered by the Keynesian fools who inhabit the Eccles Building. They are literally the Monetary Typhoid Mary of moral hazard.

That is, at this very moment heads should be rolling in the C-suites for the reckless borrowing binge of the last decade. And they would be if soaring interest rates were beginning to eat earnings alive, which with $6 trillion of debt on the S&P 500 companies alone would surely happen forthwith.

But that is not to be. The C-suites will be getting another hall pass as the Fed scoops up corporate debt by the hundreds of billions at rock bottom yields.

Plain and simple, the new corporate bond buying program will do nothing for main street; it amount to just another bailout of the 1%.

Moody’s Aaa Corporate Bond Yields, 2000-2020

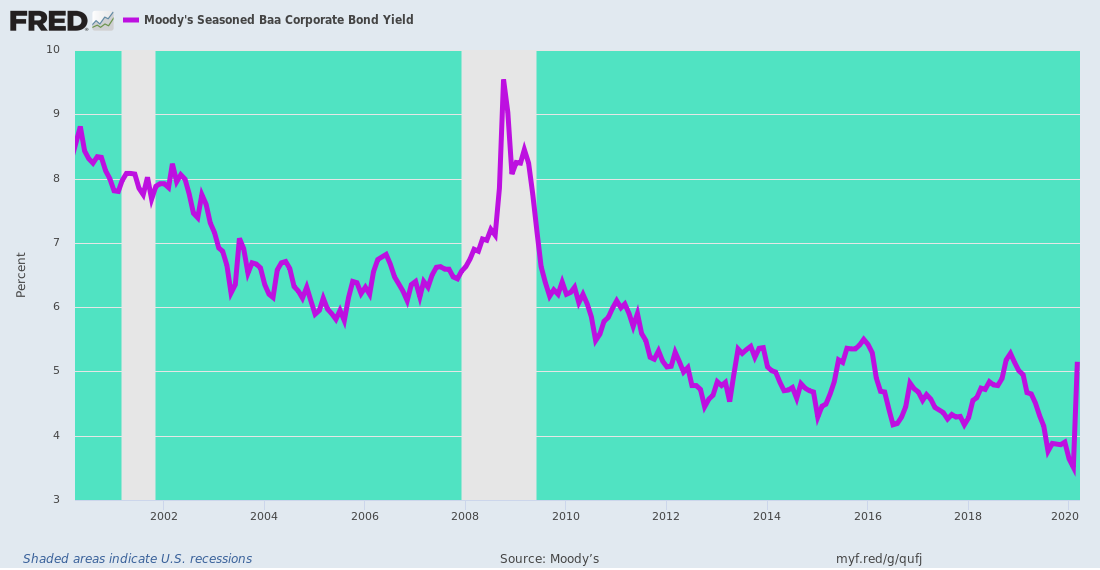

Nor is this point limited to the Aaa universe, which is small. When you look at Baa bonds, which are on the ragged edge of junk and a much larger universe of outstandings, the story is even more dispositive.

During the entire first decade of this century, the Baa yield ranged between 6% and 9%, yet economic life went on. After the massive expansion of the Fed’s balance sheet in response to the 2008 crisis, however, both the absolute yield and the spread over risk-free USTs marched ever lower.

Needless to say, this wasn’t the verdict of the free market. It was the result of asset managers becoming desperate for yield as rates on sovereign debt were being driven to the zero bound and below.

As of barely three weeks ago on March 6, therefore, the Baa yield had fallen to just 3.29%, meaning that after inflation even marginal investment grade borrowers could scoop up funds for less than 1%; and that they did with reckless abandon during the first two months of 2020.

Now, in response to the Covid-19 shock, the yield has bounced back to 5.13%, but you would think the sky has fallen based on Wall Street whining and the Fed’s blunderbuss response this AM. That is, the “recency bias” is so oppressive that a modest bounce in yields from the ludicrously low rates shown below for early March has been falsely described as a “seizure” that requires the Fed to throw all semblances of financial discipline out the window.

The Wall Street Journal’s story on the new Fed actions was reflective of this risible narrative:

The Federal Reserve will also begin lending operations to unclog corporate and municipal-debt markets, marking a major expansion of its efforts to support markets.

Really?

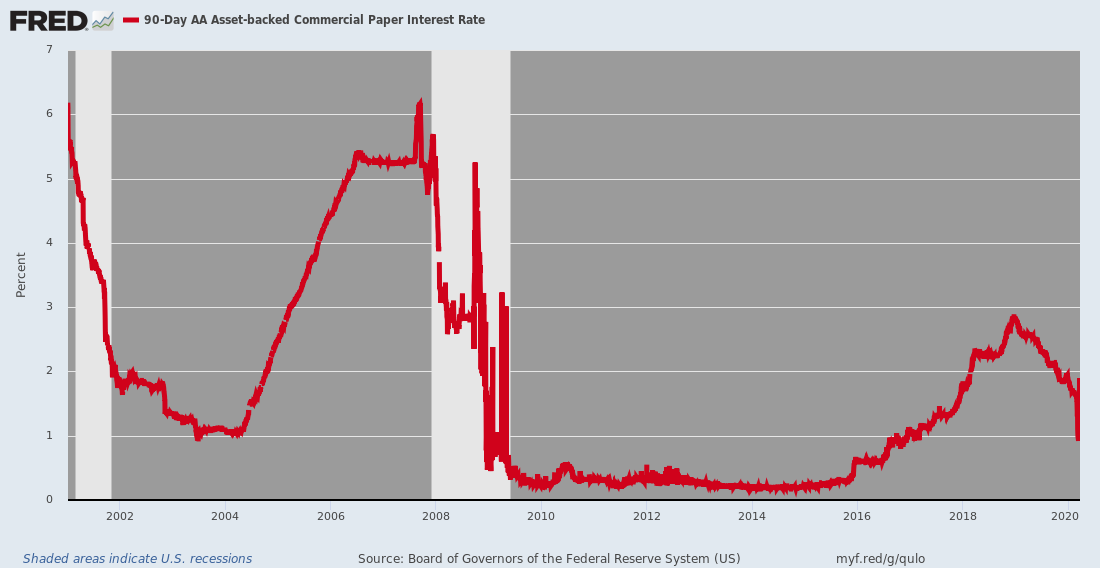

Pray tell, exactly what is “clogged” in the lower right hand side of the chart below. At this point the top of the purple bar on the right hand margin (Friday’s rate) still qualifies as yet another lower high in the saw tooth march toward the zero bound.

The same question applies to another facility, among this morning’s monetary diarrhea of lending acronyms, called TALF (Term Asset-Backed Securities Loan Facility). The latter will enable the Fed to make cheap discount loans to asset-backed securities (ABS) facilities.

This is a Wall Street concoction of debt backed by debt from the securitization mills, including

· student loans,

· auto loans,

· credit card loans,

· loans guaranteed by the Small Business Administration (SBA), and

· certain other assets.

Yet here the notion of asphyxiating any remaining trace of market based yields gets downright ludicrous. That’s because just three weeks ago on March 6th, the yield on 90-day AA Asset-backed paper of the type the Fed now will be taking as collateral was, well, 0.99%.

That’s right. The so-called “clogging” of the market has occurred because an interest rate that didn’t reflect even a full integer has blipped upwards to 2.36% as of last Friday.

Again, that’s the same number as the running core CPI inflation rate. So the crisis being addressed in this morning’s action by the Fed is to squelch an interest rate that has risen to 0.00% in real terms!

As is obvious from the chart, the Fed’s long period of pushing its short-term policy rate (e.g. Fed funds) to the zero bound between 2010 and 2016 had turned the so-called ABS market into a Wall Street venue of free stuff that would make even Bernie Sanders blush.

And now these entitled thieves want their free stuff back, and when you examine how the ABS securitization market works it’s now wonder why,

The scam works this way.

First, commercial banks make cars loans, credit card loans, student loans, small business loans etc. at rates of between 5% and 20%.

Then they slice and dice them into securitized conduits, which issue various tranches of debt, including AAA-rated slices hardly yielding 1% until the last few days. The ample difference between what they collect on the underlying loans and what they pay on the ABS securities, of course, goes into their pockets to cover losses and a hefty dose of fees and profits.

Finally, comes the cherry on top. To wit, when the originating banks sell the underlying loan paper to the ABS conduit, they get to book upfront the entire lifetime profit on the loan as a gain-on-sale!

Needless to say, we understand why banks enjoy putting the screws to hard-pressed main street borrowers and then arbitraging the profits in the Fed fostered ABS market. It’s the closet thing around to a legal printing press.

But again, if ABS rates were allowed to rise to the 4-6% yields that prevailed prior to 2008 there would be virtually no change in availability or rates for credit card, auto, student and small business loans on main street.

To the contrary, what would get whacked is the gain-on-sale profits of the Big Banks.

So what the Fed bailed out this morning by reviving the malodorous TALF facility from 2008 is nothing more than the preservation of the Wall Street economic rents that have been enabled by the Fed for years, not the Covid-19 stricken main street economy.

At an honest price, in fact, there is plenty of financing for auto, credit card and other main street loans—even without the Fed’s latest spasm of financial market free stuff.

As we said, the whores domiciled in the Eccles Building have now become truly pathetic enablers of outright Wall Street larceny.

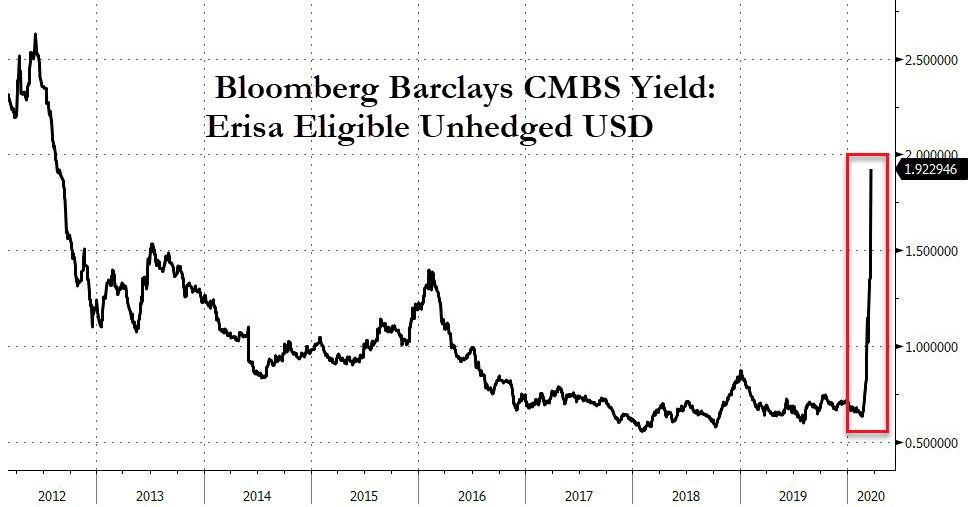

Still another bailout goodie from this morning’s monetary eruption was the addition of CMBS (commercial mortgage backed securities) to the list of “assets” eligible for purchase under the new QE5 print-a-thon.

What we are talking about here is underlying mortgages on inherently risky commercial properties like malls, office buildings, apartment complexes and warehouses. These standard 7-10 year commercial mortgages, of which there are more than $4 trillion outstanding, also get sliced and diced into various tiers of securitized paper—with the senior AAA tranche ends up bearing pint-seized yields.

As shown below, during most of the last 5 years, yields have actually hovered around just 60-80 basis points, providing a cornucopia of arbitrage profits for the banks which sell them, often to their own securitization mills.

Alas, the Fed’s draconian interest rate repression policies did obliterate yield, but they only temporarily buried risk.

As shown in the red box, the latter erupted in the CMBS markets in recent days when it suddenly dawned on the yield chasing asset managers who own this midget yield paper that the mall owners being mauled by Covid-19 might default after all—even at the so-called senior tranche level, which is precisely what happened in the residential MBS market during the great financial crisis.

So what we have is the Fed declaring the current 1.9229% yield on securitized CMBS to be an intolerable crisis, when prior to 2013 and the subsequent Fed fueled destruction of yield, it was considered all in a days work.

In fact, what we have at the top of the red box (Friday’s yield) is not a fixed income market that has seized-up or cratered at all, as the talking heads were insisting all day on bubblevision.

To the contrary, it’s just a latent risk trying to price itself. It is also occasion for

· real estate developers and speculators who have captured $100 billion or more per year of subsidized financing from the CMBS racket to catch a glimpse of what an honest bond market might actually look like; and for

· the foolish bond managers who bought this toxic waste to commence ralphing their lunch.

It’s also a beard. What we means is that there is simply is no problem in the fixed income markets that honest yields would not correct by discouraging demand and eliciting supplies of investable funds that desire to earn an adequate risk- and inflation-adjusted return.

What the Fed is really doing, of course, is bailing out the stock market, while pretending to be fixing the “plumbing” in the fixed income markets.

To be sure, it does not take a lot of investigation to understand why the Fed is so anxious to extinguish interest rates.

After all, during the last decade of financial reflation, when the nation’s financial heart-attack of September 2008 was supposedly being healed, the C-suites especially and the business community generally went on a borrowing spree that overwhelmingly funded financial engineering windfalls on Wall Street and the kind of arbitrage games described above.

Now, of course, business balance sheets are brittle and freighted down with debt service costs at the very time they are supposed to have cash reserves and resilience to what is likely to be only a short-term interruption of business activity.

To fully grasp the scam implicit in today’s Fed action, just consider why the above chart soared by 60% after the warnings of September 2008. That is, it was used for massive financial engineering ploys led by stock buybacks.

So, can the corporate C-suites use this latest gift of ultra-cheap money to pay dividends or buyback stock?

Why, yes, they can.

Well, so long as they pay a tidbit of cash interest and don’t avail themselves to the PIK option.

That’s right. These morons are saying that if the Fortune 500 companies sell investment grade debt to the Fed and then elect the payment-in-kind trick (PIK) of paying debt service with more debt, which until now has been the purview of the nether regions of the junk world, then, and only then, will they be restricted as to the use of cash raised from the Fed:

At the borrower’s election, all or a portion of the interest due and payable on each interest payment date may be payable in kind for 6 months, extendable at the discretion of the Board of Governors of the Federal Reserve System. Such interest amount will be added to, and made part of, the outstanding principal amount of the bond or loan. A borrower that makes this election may not pay dividends or make stock buybacks during the period it is not paying interest.

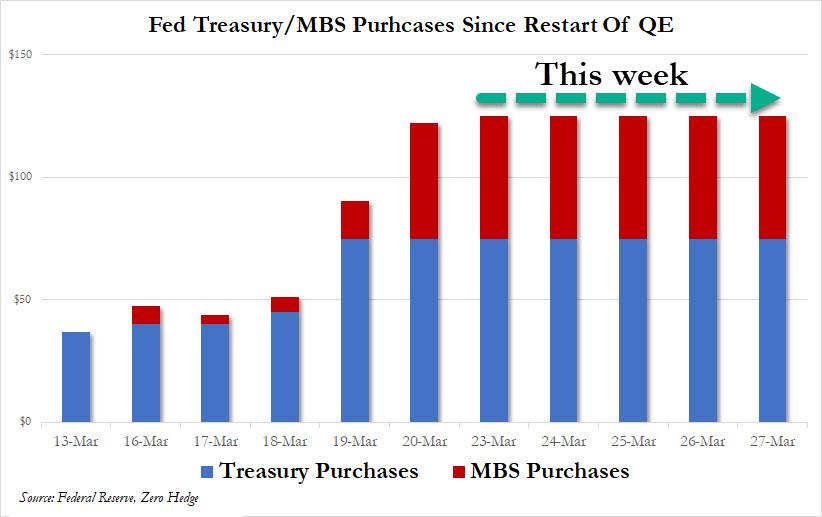

Finally, the Fed announced it intends to purchase $125 billion per day of Treasury and MBS securities during the current week, and that will require 7 separate operations just in the UST market each and every day.

The front runners are surely drooling because the Fed is announcing exactly what it will be buying, virtually by the hour.

:Needless to say, the sheer math of it is staggering. Adding this weeks massive $625 billion buy to the $374 billion of USTs and MBSs scooped up last week gets you to a mind-blowing $1 trillion of monetization in 10 trading days.

As we said: WTF?